American Express is far more than a credit card brand. In 2024, American Express credit card holders generated $1.55 trillion in spending, up 6% year over year. And in 2024 it reported a record full-year revenue of $65.9 billion, growing roughly 9–10% over the prior year.

But despite its scale, Amex still differentiates itself through selective merchant acceptance and premium customer focus. In the U.S., it maintains high satisfaction ratings — including topping the small-business card satisfaction study in 2024 with a score of 735.

For you as a merchant, it’s crucial to have the right infrastructure in place to accept Amex payments, since many of your customers will already carry an American Express card.

JIM provides one straightforward solution — letting you accept Amex payments directly from your iPhone without the heavy lifting of hardware or the burden of expensive installation costs. More about how to accept Amex payments and what it means for your business is covered below.

What is American Express?

American Express (Amex) is a global leader in credit card payments and financial services, best known for its premium brand, loyal customer base, and higher-than-average transaction volumes. Unlike Visa or Mastercard, which primarily operate as card networks, American Express often acts as both the issuer and the network. This “closed-loop” model gives Amex unique control over its ecosystem — from setting fees to shaping customer experience and merchant tools.

For merchants, this distinction matters. Amex cardholders consistently spend more per transaction than customers using other major cards, and many are frequent travelers, business clients, or high-income individuals. Accepting Amex can signal that a business is positioned to serve those valuable customers. However, in some regions where local payment options dominate — such as iDEAL in the Netherlands or Girocard in Germany — American Express isn’t the market leader. Yet globally, it remains a giant in the card industry, driving trillions in annual spending and ranking as a must-have for businesses aiming to serve international clients.

To understand how American Express fits into your business strategy, it’s important to look at its different services — from business credit cards to merchant solutions and rewards programs.

Credit and charge cards

Amex offers both Amex credit cards and traditional charge cards. Charge cards require balances to be paid in full each month, but they typically come with higher limits and attractive perks. For merchants, these products mean customers are less constrained by short-term budgets, often resulting in larger average ticket sizes. Credit cards, meanwhile, give customers flexibility while keeping them loyal to Amex. Both product types connect merchants to a segment of customers who expect premium service and are willing to spend more.

Digital services

American Express has invested heavily in digital infrastructure. Beyond its physical cards, Amex is fully compatible with Apple Pay, Google Pay, Samsung Pay, and its own Amex mobile app. This makes it easy for merchants to accept contactless American Express payments both online and in-store, without requiring complex hardware. As consumers shift toward mobile and digital wallets, this flexibility ensures merchants stay relevant at checkout and meet customer expectations for speed and security.

Merchant services

Amex provides more than payment acceptance — it offers a suite of merchant services designed to create value. These include advanced fraud detection, chargeback management, and detailed transaction insights. Merchants can also tap into Amex’s marketing programs, which highlight participating businesses to Amex cardholders, driving new customers through targeted promotions. This ecosystem positions Amex as not just a payment processor but also a partner in customer acquisition and retention.

Business financing

Recognizing that merchants often need more than just payment processing solution, Amex provides financing tools such as working capital loans, merchant financing programs, and lines of credit. These services are designed to help businesses manage cash flow, purchase inventory, or expand operations without relying on separate financial institutions. By combining online payments and financing under one umbrella, Amex reduces complexity for merchants and builds stronger long-term relationships.

Membership Rewards

The Membership Rewards program is one of Amex’s strongest differentiators. Cardholders earn points with every purchase, redeemable for travel, shopping, or statement credits. For merchants, this translates into customers who are motivated to spend more where Amex is accepted, since every transaction helps them reach rewards faster. Businesses that accept Amex effectively align themselves with a powerful loyalty engine, increasing both transaction frequency and basket size.

Where is American Express mostly used?

American Express has built strong footing in high-income, credit-friendly markets, but its adoption varies significantly depending on local payment culture, merchant cost sensitivity, and regulatory environments. Globally, Amex is accepted at 160 million merchant locations as of its latest growth disclosures. In its home market, the U.S., Amex is especially ubiquitous — it is accepted at 99 % of U.S. merchants that take credit cards.

However, outside the U.S., its acceptance is less uniform. In parts of Europe, Asia, and Latin America, local or regional payment rails (like domestic debit networks, bank-based schemes, or QR payments) tend to dominate. In those places, merchants may be more reluctant to onboard Amex due to perceived higher transaction costs and complexity.

Culturally, in markets where consumers prefer local or familiar global payments and where credit card penetration is lower, Amex faces steeper barriers. But in business travel hubs, luxury retail centers, and tourism-heavy locales, Amex often “punches above its weight” — prized by tourists and high spenders who expect to use premium cards.

Why should businesses accept Amex payments?

If you want to fully serve your target customers, you can’t afford to omit American Express. Many affluent, frequent-traveler, and premium-segment customers expect to use Amex — and if you don’t offer it, you risk losing business or eroding trust. That’s why your payment stack must include solutions that support how to accept Amex payments seamlessly, reliably, and cost-efficiently.

Below are several core benefits for merchants who adopt Amex acceptance:

- Access to high-spending customers: Amex cardholders tend to have higher purchase power and spend more per transaction. By accepting Amex, you unlock a customer segment that might otherwise bypass your store or checkout in favor of a competitor that does support it.

- Increased transaction value and frequency: Customers using premium cards often make larger and more frequent purchases. Supporting Amex can push up your average order value and repeat purchase rates.

- Marketing leverage and visibility: As an Amex-accepting merchant, you may be eligible for co-marketing programs, “Amex Offers,” or placement in Amex’s merchant directories and cardholder communications — exposing your business to new potential customers.

- Trust and brand credibility: Accepting Amex signals a level of professionalism, global readiness, and customer service orientation. For many consumers, seeing the Amex logo reassures them about payment security and legitimacy.

- Robust merchant tools and support: American Express offers merchant dashboards, fraud prevention tools, dispute management, and reporting features aimed at helping merchants manage risk and operations more effectively.

How to accept Amex payments? step-by-step guide

Traditionally, getting started with Amex payments has meant significant upfront investment: you need to install specialized POS terminals, integrate with payment networks, and often pay setup or certification costs. Many merchants hesitate because hardware and certification can cost hundreds to thousands of dollars depending on your size and region.

But the landscape is changing. There are now hardware-free alternatives like JIM that let you accept Amex payments via smartphone — no bulky terminal, no costly installation, and minimal setup. This modern approach makes “how to accept Amex payments” far more accessible, especially for small or mobile businesses.

Below, we describe both the traditional route and the modern, no-hardware method so you can choose the option that fits your business best.

Step 1: Open a merchant account

You’ll need a merchant account that supports American Express (often via an acquirer or payment provider). You can start at the American Express “Getting Started” page to enroll: set up your business profile, submit required documentation, and link your bank account.

Step 2: Obtain an Amex-compatible device or system

To accept payments in-person, you’ll typically need a POS terminal, card reader, or virtual terminal that supports EMV/contactless transactions and is certified for Amex. Make sure it supports chip, NFC, and magnetic stripe as needed.

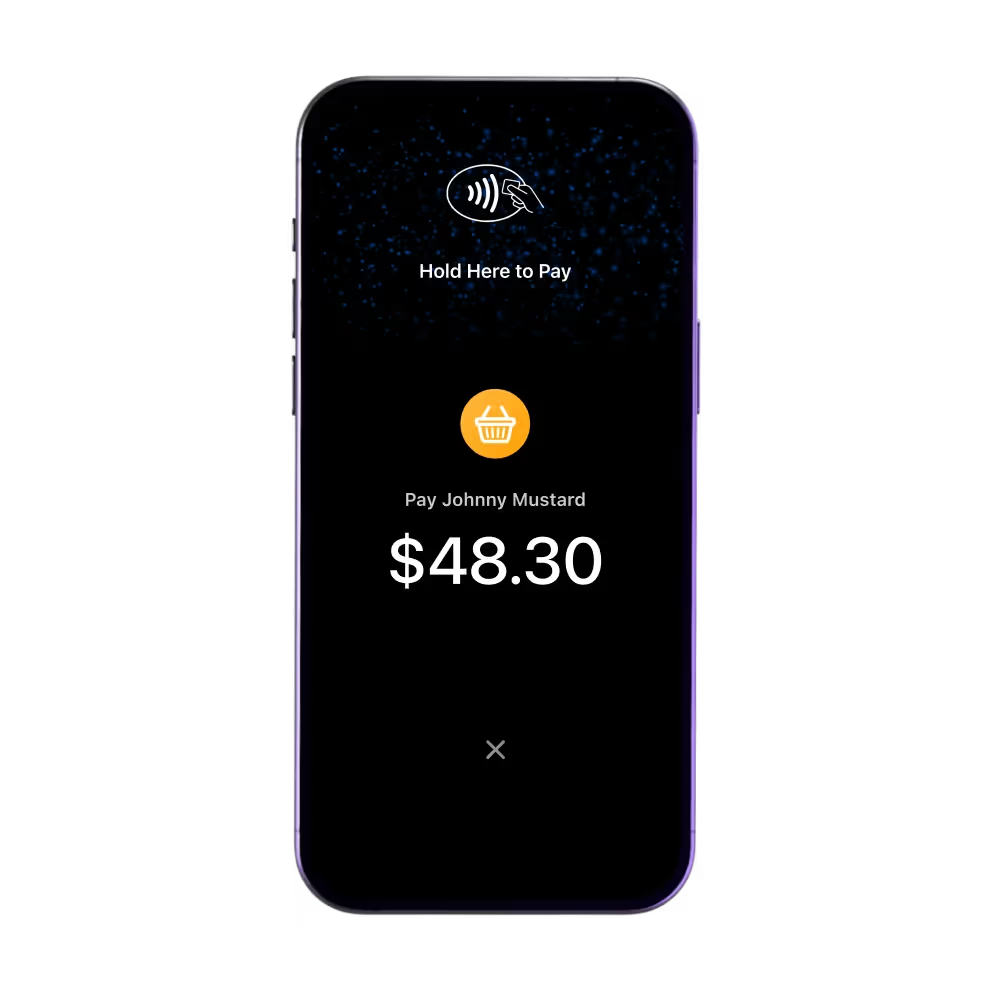

JIM: No-hardware way for accepting Amex payments

Alternatively, you can skip equipment altogether using a mobile app solution like JIM. With JIM, you accept Amex payments via smartphone in a three simple steps:

- When making a sale, open JIM, tap the sales amount, and ask your buyer to tap to pay.

- Receive your funds in seconds onto your JIM debit card paying only a 1.99% flat fee - regardless of the transaction amount.

Step 3: Maintain PCI DSS compliance

Because you are handling cardholder data, you must comply with PCI DSS — a global standard protecting card data during processing, storage, or transmission. Depending on your transaction volume and setup (physical terminal, cloud gateway, mobile app), your compliance requirements vary (self-assessment questionnaire, external audit, etc.).

Is American Express safe?

Yes — American Express invests heavily in security to protect both merchants and cardholders. Below is a summary of key safeguards and how they apply to your business.

Key security layers and protections of Amex include:

- PCI DSS compliance: American Express requires all merchants and service providers to adhere to the PCI DSS standard, which sets out requirements for protecting cardholder data, securing networks, access control, monitoring, and incident response.

- Tokenization: Amex replaces sensitive card information (like the PAN) with tokens in digital and mobile transactions. This reduces exposure to data breaches and lowers your scope of handling raw payment credentials.

- SafeKey (3-D Secure): For online transactions, Amex uses SafeKey — its implementation of EMV 3-D Secure — which adds authentication steps (e.g. verification codes) when needed. This helps reduce fraud, lowers liability for authenticated chargebacks, and enhances customer trust. In 2024, Amex upgraded to SafeKey 2.3 to support newer device types and stronger authentication protocols.

- Advanced fraud and risk analytics: Behind the scenes, Amex uses real-time algorithms and behavioral analysis to flag suspicious transactions. This helps block or challenge high-risk activity before damage occurs.

- Regulatory alignment and multifactor authentication: In markets with strong regulatory requirements (such as under PSD2 in Europe), Amex supports necessary multi-factor authentication and strong customer authentication flows. SafeKey and related tools are part of that compliance strategy.

Start accepting Amex payments easily

Accepting American Express used to mean big upfront investment — special terminals, network certifications, and messy integrations. Many merchants skipped it, seeing Amex as too complex or costly. But that’s changing: JIM make it possible to accept Amex payments right from your phone, without the heavy hardware or installation.

With JIM, you can get started in minutes: download the app and start accepting payments. No terminals, no mess.

.avif)