You're about to sign up for Square, but something makes you pause. Maybe it's the variable pricing structure, the delayed payouts, or the stories you've heard about frozen accounts.

Square pioneered mobile payments for small businesses, but today's market offers alternatives with faster payouts, transparent pricing, and features tailored to specific business models. Mobile point-of-sale payment transaction values continue growing year-over-year, driving innovation across the payment processing industry. This growth means more options for small businesses, from instant-payout solutions to developer-focused platforms and comprehensive POS systems.

Choosing the right payment processor affects your daily cash flow, processing costs, and customer checkout experience. This guide breaks down the top Square alternatives and helps you match payment technology to your actual business needs.

What Is Payment Processing Software?

Payment processing software is the technology that moves money from your customer's card or digital wallet into your bank account. It coordinates the complex handoff between card networks, banks, and financial institutions that happens every time someone taps, swipes, or clicks to pay.

This is different from a payment processor (the company that handles transaction routing) or a payment gateway (the technology that encrypts and transmits card data). It's also distinct from a merchant account, which is the specialized account where funds settle before reaching your business bank account. Payment processing software brings these pieces together into a functional system you can actually use.

At its core, this software serves as the bridge between a customer saying "I want to pay" and you seeing money in your account. The best payment solutions handle authorization, fraud screening, settlement, and reporting while integrating with the rest of your tech stack.

How Does Payment Processing Software Work?

Understanding the transaction flow helps you evaluate which payment processing systems fit your needs. Here's what happens when a customer pays with a card.

Step 1: Payment initiation. The customer presents their credit card, debit card, or digital wallet at your point of sale or online checkout. The payment software captures the card data and encrypts it immediately.

Step 2: Gateway transmission. The payment gateway routes the encrypted transaction to your payment processor. For online payments, this happens through API connections; for in-person payments, it occurs through NFC readers or card terminals.

Step 3: Network routing. Your processor forwards the request to the appropriate card network (Visa, Mastercard, American Express) based on the card type. The network then contacts the customer's issuing bank.

Step 4: Authorization. The issuing bank checks the customer's available balance, fraud signals, and account status. Within seconds, it sends an approval or decline back through the same chain.

Step 5: Settlement. Once approved, the acquiring bank (your merchant bank) requests funds from the issuing bank. After interchange fees and processing costs are deducted, the remaining amount settles to your merchant account. Traditional systems batch these transactions and settle in one to three business days; some modern solutions offer real-time or same-day settlement.

Core Features of Payment Processing Software

Payment processing software varies widely in functionality. Understanding the core features helps you identify what you actually need versus what you're paying for but never using.

Payment Acceptance

The foundation of any payment system is accepting the payment methods your customers prefer. Modern software handles credit and debit card processing, digital wallets like Apple Pay and Google Pay, and both in-person and online payments. Some platforms also support ACH transfers, buy-now-pay-later options, and international payment methods, depending on your customer base.

Payment Gateway Integration

For online businesses, gateway integration determines how payments flow from your website or app to the processor. Strong API connectivity allows developers to customize checkout experiences, while pre-built integrations connect to popular e-commerce platforms without code. The gateway encrypts sensitive card data and ensures transactions meet security standards.

Security and Fraud Protection

Payment processing software must meet PCI DSS compliance standards to protect cardholder data. Look for tokenization (which replaces card numbers with meaningless tokens), end-to-end encryption, and fraud prevention tools that flag suspicious transactions before they complete. Chargeback management features help you respond to disputes and track patterns that might indicate fraud.

Reporting and Analytics

A clear transaction dashboard shows what's happening with your money in real time. Sales tracking and reporting help you understand revenue patterns, while cash flow visibility lets you plan around settlement timing. The best software makes this data accessible without requiring you to export everything to a spreadsheet.

Integration Capabilities

Payment processing rarely exists in isolation. Integration with accounting software like QuickBooks automates reconciliation and reduces manual entry. Connections to your POS system, ecommerce platform, and CRM create end-to-end workflows that save hours of administrative work each week.

Automation Features

Recurring billing handles subscriptions and memberships without manual intervention. Payment links let you request payment via text or email without building a full checkout page. Automated workflows can trigger invoices, send receipts, and update inventory when transactions are complete.

Types of Payment Processing Software

Different business models require different payment approaches. Understanding the main categories helps you narrow your search.

All-in-One Payment Platforms

These platforms bundle payment processing, gateway services, and merchant accounts into a single package. Stripe and Square are well-known examples. They work well for businesses that want one provider handling everything, though they may lack specialized features for specific use cases. Pricing is typically straightforward, but you're locked into their ecosystem.

Specialized E-commerce Solutions

Some software focuses specifically on online payments, offering deep integrations with shopping carts, subscription management, and digital product delivery. These solutions optimize conversion rates and checkout flow for web-based businesses but may not handle in-person payments well.

Mobile Payment Solutions

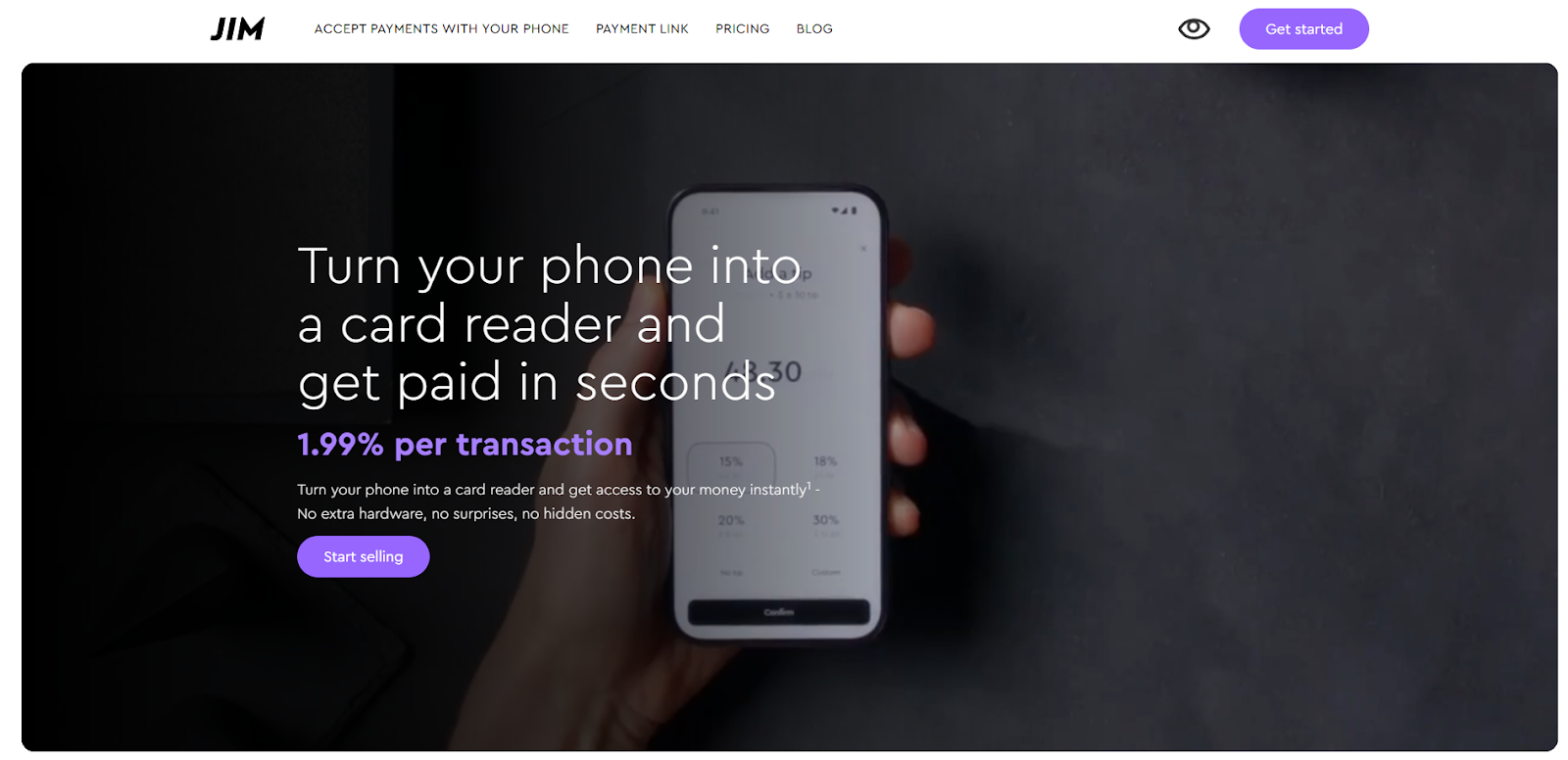

For businesses that sell on the move, mobile payment solutions prioritize portability and simplicity. Tap to Pay technology lets you accept contactless payments directly on a smartphone without external hardware. Food trucks, farmers market vendors, and service providers who travel to clients benefit from this flexibility. JIM falls into this category, designed specifically for mobile in-person payments.

Enterprise Payment Systems

Larger operations need advanced functionality: multi-location management, custom reporting, complex fee negotiations, and dedicated account managers. Traditional processors like Global Payments (formerly TSYS) serve this market. These systems offer powerful capabilities but come with higher complexity, longer implementation timelines, and costs that don't make sense for most small businesses.

Payment Processing Software Examples

Payment processing software plays a central role in how businesses accept, manage, and reconcile payments across channels. From in-person card transactions to online and mobile payments, the right platform affects costs, speed, security, and customer experience. Below are several payment processing software examples that illustrate how different tools support different business needs and use cases.

JIM

JIM takes a mobile-first approach focused on in-person payment acceptance. The flat 1.99% fee applies regardless of card type, with no monthly charges or hardware purchases. Instant settlement means funds reach your JIM Visa® Prepaid Card in seconds rather than days. For mobile businesses, market vendors, and service providers who primarily accept payments face-to-face, this simplicity and speed address real pain points.

Stripe

Stripe built its reputation serving developers and online businesses. The API-first approach allows extensive customization, and the documentation is among the best in the industry. Stripe handles online payments, subscriptions, and marketplace payouts. Pricing runs around 2.9% plus $0.30 per online transaction, with volume discounts available. It's a strong choice if you have technical resources and primarily sell online.

PayPal

PayPal's brand recognition creates trust at checkout, which can improve conversion rates for online stores. Business accounts offer invoicing, payment processing services, and integration with major e-commerce platforms. Fees vary by transaction type but typically range from 2.9% to 3.49% plus fixed fees. The familiarity factor matters for certain customer bases, though fees tend toward the higher end.

Square

Square combines POS hardware with online payment processing and business management tools. The ecosystem includes registers, terminals, and readers alongside software for appointments, payroll, and inventory. Processing fees are typically 2.6% plus $0.10 for in-person payments. Square works well for businesses that want hardware and software from one provider and don't mind buying into their ecosystem.

Global Payments (TSYS)

Global Payments serves larger merchants and enterprises with traditional processor services. They offer interchange-plus pricing, dedicated account management, and solutions for complex payment needs across multiple locations or high transaction volumes. This approach fits businesses processing significant volume who can negotiate rates, but the complexity doesn't suit most small operations.

Pros and Cons of Payment Processing Software

Before choosing a payment processing platform, it’s important to weigh the advantages and trade-offs involved. Payment processing software can streamline transactions, improve cash flow visibility, and enhance the customer checkout experience, but it may also introduce fees, technical dependencies, or compliance considerations. The pros and cons below highlight the key benefits and potential drawbacks to help you evaluate whether a solution aligns with your business needs.

Pros:

- Streamlined acceptance across channels: Accept credit cards, debit cards, and digital wallets, whether customers pay in person or online, all through one system.

- Real-time transaction visibility: See payments as they happen rather than waiting for batch reports, giving you clearer insight into daily sales.

- Automated reconciliation: Transactions sync with accounting software, reducing the manual work of matching payments to invoices.

- Enhanced security and fraud protection: Built-in tokenization, encryption, and fraud screening protect both you and your customers.

- Improved customer experience: Fast, reliable checkout builds trust and encourages repeat business.

- Better cash flow management: Understanding when funds settle helps you plan expenses and avoid overdrafts.

Cons:

- Processing fees accumulate: Even small percentages add up at volume. A business processing $50,000 monthly at 2.9% pays over $17,000 annually in fees.

- Integration complexity: Connecting payment software to your existing tech stack sometimes requires developer resources or compromises.

- Platform lock-in: Switching providers means migrating customer data, updating integrations, and retraining staff.

- Staff onboarding takes time: New systems have learning curves, and mistakes during the transition can frustrate customers.

How to Choose the Right Payment Processing Software

Choosing payment processing software goes beyond comparing transaction fees or brand recognition. The following considerations outline what to evaluate when selecting a solution that supports both current needs and future growth.

Assess Your Business Needs

Start by identifying how you actually accept payments. Do you sell primarily in-person, online, or both? What's your average transaction size and monthly volume? Some industries have specific requirements (restaurants need tip adjustments; subscriptions need recurring billing). Consider where you expect to be in two years, not just where you are today.

Compare Pricing Models

Flat-rate pricing (like 2.9% per transaction) is predictable but may cost more at volume. Interchange-plus pricing passes through actual card costs plus a markup, which can be cheaper but harder to predict. Look beyond the headline rate: monthly fees, PCI compliance charges, chargeback fees, and hardware costs all affect total expense. Settlement speed impacts cash flow, so factor in whether waiting three days for funds creates problems.

Evaluate Integration Requirements

Check compatibility with your current tech stack. Does the software offer API access if you need custom development? Can it connect to QuickBooks or your preferred accounting software? If you sell online, verify it integrates with your e-commerce platform. Gaps in integration mean manual work.

Check Security and Compliance

Confirm PCI DSS certification and understand what compliance responsibilities remain with you versus the provider. Review fraud prevention tools and chargeback handling processes. Ask how the platform protects customer data and what happens if a breach occurs.

Consider Customer Support

Problems with payments need fast resolution. Check whether support is available 24/7 or only during business hours, and through what channels. Evaluate onboarding assistance, training resources, and technical documentation quality. Reading reviews about support experiences often reveals more than sales materials.

Test User Experience

The dashboard should make sense without a training course. Mobile app functionality matters if you accept payments away from a desk. Walk through the checkout flow from your customer's perspective. Clear reporting saves time; confusing reports create work.

Industry-Specific Considerations

Different businesses face different payment challenges. Food trucks and mobile vendors need portability above all, processing payments wherever they set up without reliable wifi or power. Coffee shops and cafes prioritize speed, moving customers through quickly during rush periods. E-commerce businesses focus on optimizing online payment conversion and reducing cart abandonment. Service providers like tutors and contractors often need payment links and invoicing more than full checkout systems.

Making Payment Processing Work for Your Business

Choosing payment processing software isn't about finding the perfect solution. It's about matching technology to the way you actually work. A coffee shop processing hundreds of small transactions daily has different needs than a consultant sending occasional invoices. An online boutique requires different functionality than a barber shop accepting walk-in payments.

Focus on three priorities: transparent pricing that won't surprise you, settlement speed that supports your cash flow, and ease of use that doesn't require a manual every time you process a payment. The right payment solution feels invisible to you and effortless to your customers.

Whether you need the developer flexibility of Stripe, the ecosystem approach of Square, the enterprise capabilities of Global Payments, or the mobile simplicity of JIM, the best choice is the one that removes friction from getting paid. Everything else is secondary.

Ready to simplify in-person payments? Explore JIM's Tap to Pay and see how turning your iPhone into a payment terminal eliminates hardware costs and settlement delays.

.avif)